At the heart of every investment firm, you’ll find a highly specialized finance function. Their role is diverse. From maintaining the integrity of a fund’s books, calculating net asset value (NAV), coordinating audits and tax filings, to producing the financial reports that investors rely on to assess performance.

An internal team does more than safeguard the integrity of the fund’s records. Since they’re absorbed in the firm’s culture, strategic alignment and control become easy. They also make collaboration seamless, especially within different departments like investment deal teams and finance.

Operating within the firm provides them with direct insight into the fund’s strategy, deal pipeline, and investor engagement. This makes collaboration easier and makes room for need-based operations and investment strategies.

For these reasons, the debate around fund administration should not be an either-or scenario. We cannot assume that internal finance teams are inefficient or obsolete, and easily replaceable through outsourcing. Quite the opposite. They play a central role in shaping investor trust, interpreting portfolio dynamics, and communicating the strategy behind the numbers. Any discussion of outsourcing must start by recognizing these capabilities. Excellence in relationship management, contextual interpretation, and narrative clarity. The area where in-house teams deliver their greatest value.

When Scale Changes the Operating Priorities

As funds grow, the operating environment changes quickly. You realize you now have more LPs, additional vehicles, feeder structures, and even co-investments. Since these didn’t exist in the earlier stages, they introduce new layers of administrative complexity. Reporting cycles become more demanding, data flows multiply, and finance teams must manage increasingly sophisticated accounting and regulatory requirements.

At the same time, LP expectations rise. Institutional investors now expect faster reporting, greater transparency, and consistent data across vehicles. Studies show that Operational Due Diligence (ODD) plays a central role in the institutional investment process. Beyond reviewing governance and operational controls, investors now place significant weight on the timeliness and quality of fund reporting, viewing it as a critical signal of operational discipline and transparency.

With more demands from investors, internal finance teams are forced to change their daily operations. More attention is given to operational tasks such as NAV production, reconciliations, capital call processing, and regulatory reporting. As most alternative managers scale operations, you’ll most likely come across this common pressure point caused by a growing administrative load.

The result is a subtle but important trade-off: internal teams spend more time managing operational workflows and less time focusing on investor engagement and performance storytelling. Yet, investor engagement is the area where their proximity to the portfolio and LP relationships creates the most value.

The Operational Layer Fund Administration Is Built to Handle

Fund administration exists to manage the operational infrastructure of a fund. These are the processes that must run consistently and accurately behind the scenes. Fund admin tasks include capital call processing, NAV calculations, investor allocations, portfolio and cash reconciliations. They’ll also handle audit preparation and the production of LP capital account statements. Investors may not care, or even know about these functions, but they form the backbone of reliable fund operations.

As funds scale, these processes evolve into highly structured workflows from occasional finance tasks. NAV production, for example, often requires multiple valuation inputs, portfolio-level adjustments, waterfall calculations, and investor-level allocations. Capital calls and distributions must be executed with precision across potentially hundreds of LPs, each with its own commitments, side-letter terms, and reporting expectations.

This is precisely the layer fund administrators are designed to handle. Their operating models focus on repeatable financial processes, structured controls, and scalable reporting frameworks.

Additionally, as private market assets grow, regulatory scrutiny increases. It therefore becomes good practice for managers to increasingly rely on specialized operational partners to manage these administrative workflows efficiently and consistently.

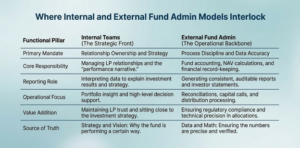

Where Internal and External Fund Admin Models Interlock

The strongest operating models in private markets are not built on a strict choice between in-house and outsourced administration. Instead, they divide responsibilities clearly. Internal teams retain ownership of LP relationships, portfolio insight, and the performance narrative. Outsourced fund administrators focus on the operational backbone. They perfectly handle fund accounting, NAV calculations, reconciliations, capital calls, and investor reporting.

This separation reflects the natural strengths of each side. Internal teams sit closest to the investment strategy and investor base, making them best positioned to explain performance and maintain LP trust. Fund administrators, meanwhile, are structured around process discipline and data accuracy. This ensures financial records, allocations, and reporting outputs remain consistent and auditable.

Industry analysis shows that alternative asset managers adopt this hybrid model precisely to balance investor engagement with operational scale. In fact, more than 75% of alternative fund managers already use a third-party administrator. The main drivers include cost reduction, talent scarcity, scalability, and focus on investment performance

Rather than overlapping, the in-house and outsourced fund admin roles interlock. Administrators maintain the integrity of the financial data, while internal teams interpret that data for investors. In practice, this allows operational rigor to support stronger investor communication. The people managing LP relationships are not pulled away by the mechanics of fund administration.

The Investor Payoff: Why Operational Excellence Becomes Front-Facing

A 2025 study shows that 80% of wealth managers consider client experience a primary competitive advantage. When the operational layer runs smoothly, the biggest beneficiary is the investor, not the back office. With fund accounting, reconciliations, and reporting workflows handled consistently, internal teams regain the time and focus needed to engage LPs more proactively. They concentrate on what investors actually experience: timely communication, thoughtful performance explanations, and responsive answers to complex portfolio questions.

This matters because institutional investors increasingly evaluate managers not only on returns, but also on operational transparency and reporting quality. As we’ve seen, communication practices are now central elements of operational due diligence. LPs want clarity around valuation movements, portfolio exposure, and the drivers behind performance.

In that sense, operational excellence becomes a front-facing advantage. Accurate, well-structured reporting creates the foundation that allows internal teams to deliver stronger investor engagement. With reliable data and disciplined processes in place, finance and investor relations teams can shift their attention to interpretation, context, and relationship management. These areas ultimately shape how LPs experience the fund.

Ready to bridge the gap between back-office operations and investor relations? Discover how the RAISE platform creates a seamless operational layer for your fund. Book a Technical Walkthrough.